SMM, January 7:

As of this Tuesday, at northern ports: Australian lump ore was priced at 41.5-42 yuan/mtu (flat WoW); Australian fines at 38-38.5 yuan/mtu (flat WoW); South African semi-carbonate at 33.5-34 yuan/mtu (up 1.50% WoW); Gabonese ore at 38-38.5 yuan/mtu (up 1.32% WoW); South African high-iron ore at 28.5-29 yuan/mtu (flat WoW). At southern ports: Australian lump ore was priced at 43.5-44 yuan/mtu (flat WoW); Australian fines at 39-39.5 yuan/mtu (flat WoW); South African semi-carbonate at 34-34.5 yuan/mtu (flat WoW); Gabonese ore at 40.5-41 yuan/mtu (up 1.24% WoW); South African high-iron ore at 29-29.5 yuan/mtu (flat WoW).

Currently, miners' quotations remain firm, while downstream alloy plants are cautious in their purchases, keeping the manganese ore spot market stable. Regarding the outlook for imported manganese ore prices, overall market sentiment is optimistic. Specifically, most industry participants are bullish on future manganese ore prices, mainly due to the tight spot supply of some mainstream manganese ore varieties, active market inquiries, and miners' reluctance to sell at low prices. Additionally, the destocking pace of manganese ore inventories at ports has accelerated, alloy plants have winter stockpiling demand, downstream demand support has strengthened, and miners' quotations remain firm.

On the other hand, some industry participants are bearish on manganese ore prices, primarily because the supply surplus of manganese ore at northern ports persists, northern alloy plants remain cautious in their manganese ore purchases, and their acceptance of high-priced manganese ore is low. Furthermore, the operating rate of southern alloy plants remains at a low level, leading to weak manganese ore purchasing demand.

A small number of industry participants believe that manganese ore prices will remain stable, mainly because the total inventory of manganese ore at ports is sufficient, and downstream alloy plants, due to production pressure, tend to bargain down purchasing prices and show weak willingness to purchase high-priced manganese ore. The tug-of-war between supply and demand for manganese ore suggests that prices are expected to remain stable in the future.

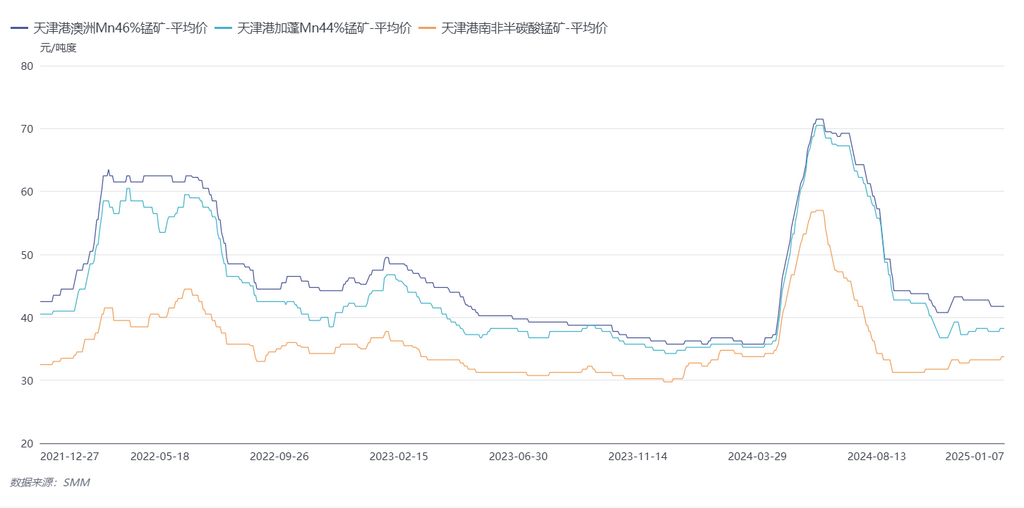

》Subscribe to view historical price trends of SMM manganese products

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)